Backtesting Trading Strategies: A Complete Guide (2026)

Backtesting Trading Strategies: A Complete Guide (2026)

Most traders skip backtesting and pay for the lesson with their account. Backtesting lets you stress-test a strategy across hundreds of trades before risking a single dollar, turning months of live losses into a weekend of research. This guide breaks down the full process, from defining rules that leave zero room for guesswork to spotting the overfitting traps that make backtests look great on paper and fall apart in real markets.

class SampleComponent extends React.Component {

// using the experimental public class field syntax below. We can also attach

// the contextType to the current class

static contextType = ColorContext;

render() {

return <Button color={this.color} />

}

}

Last Updated: June 2, 2026

Backtesting is the process of applying a trading strategy to historical market data to measure how it would have performed. You define exact entry and exit rules, run those rules against past price data across hundreds of trades, and calculate key metrics like win rate, profit factor, expectancy, and maximum drawdown. A strategy that produces positive expectancy over 200+ backtested trades gives you statistical evidence of an edge. A strategy that doesn't eliminates itself before you lose real money.

Backtesting is how you answer the most important question in trading: does this strategy actually work? Instead of risking real money to find out, you run your setup against historical data and measure the results. If the strategy produces a positive expectancy across hundreds of trades, you have evidence of an edge. If it doesn't, you've saved yourself months of losses.

Every consistently profitable trader backtests. Not because it guarantees future results (it doesn't), but because it eliminates strategies that have no historical basis. A strategy that loses money over 500 backtested trades isn't suddenly going to work when you trade it live. Backtesting compresses years of market experience into days of research.

This guide walks through the full backtesting process: defining your strategy, choosing your data, running the test, interpreting results, and avoiding the pitfalls that make backtests unreliable.

TL;DR

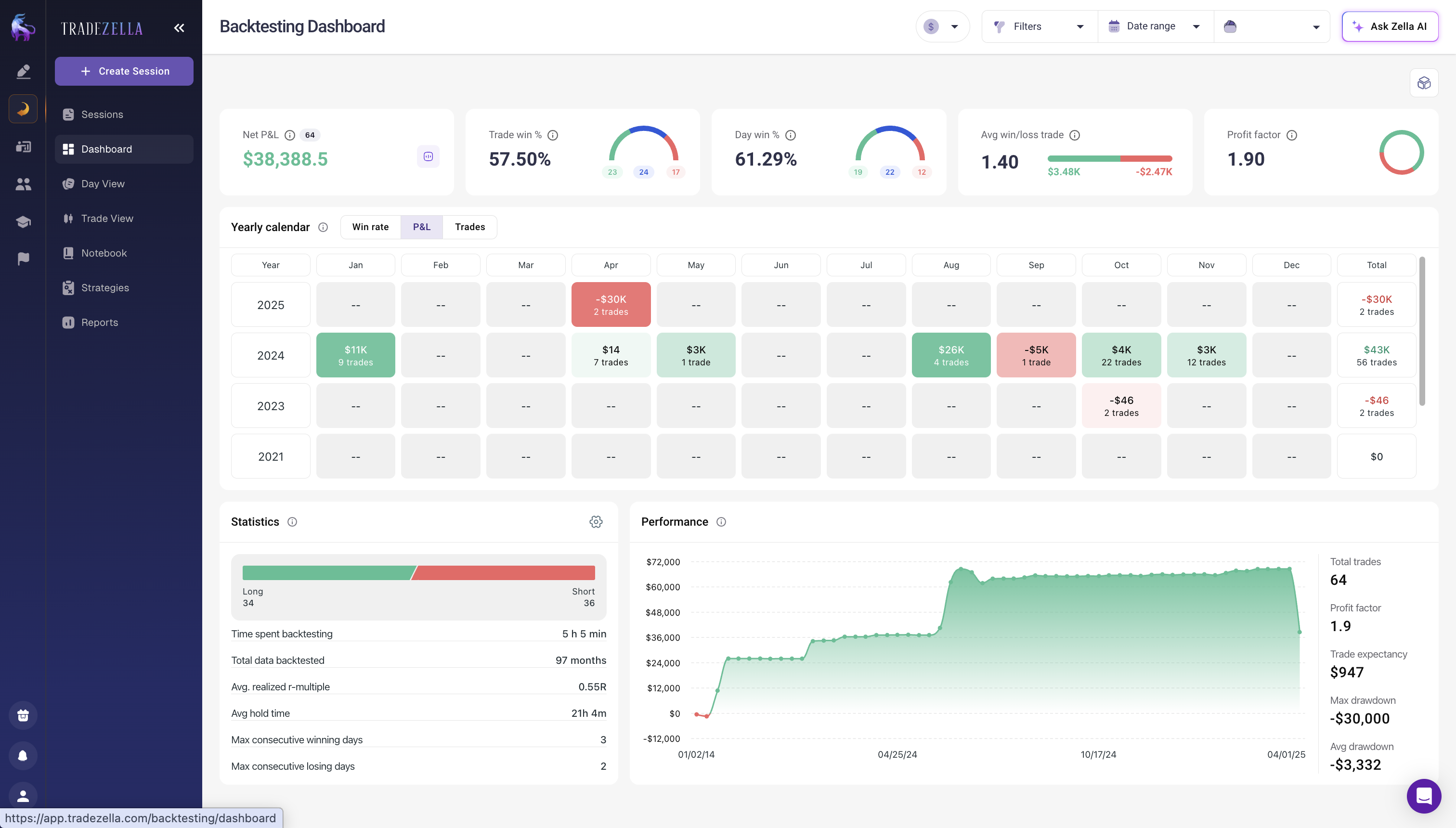

Backtesting means running your trading strategy against historical data to see if it works before you risk real money. Define exact rules, test across 100+ trades and multiple market conditions, then validate with out-of-sample data. A profit factor above 1.5 and positive expectancy across 200+ trades gives you evidence of an edge. TradeZella's backtesting engine runs with 11+ years of data, built-in ICT indicators, auto-journaling for every backtested trade, and 50+ analytics reports that let you compare backtest results against live performance in the same dashboard. TradeZella also offers automated no-code backtesting where traders describe strategies in plain English and see every individual trade the engine executed, with Zella AI analysis on every session, along with scenario backtesting with pre-built strategy templates that let you practice specific setups on targeted historical conditions.

What Does Backtesting Actually Prove?

Backtesting proves that a strategy had an edge in the past. It doesn't guarantee that edge will persist. Markets change, volatility regimes shift, and what worked in 2022 might not work in 2026. But here's why it still matters:

A strategy with no historical edge has no basis for live trading. You're guessing. A strategy with a documented edge across multiple market conditions gives you a foundation to build on. It won't be exactly right going forward, but it won't be randomly wrong either.

What Backtesting Tells You

Win rate for your specific setup over a meaningful sample (100+ trades).

Average win size versus average loss size (your reward-to-risk ratio).

Expectancy: the average amount you'd expect to make per trade over time.

Maximum drawdown: the worst peak-to-trough decline your strategy experienced historically. This number becomes the foundation of your drawdown management protocol. If your backtest shows a 15% maximum drawdown, you know your Tier 3 threshold needs to accommodate that.

Profit factor: gross profits divided by gross losses. Anything above 1.5 is solid.

What Backtesting Doesn't Tell You

How the strategy performs in future market conditions.

Whether you can actually execute it with discipline. FOMO, revenge trading, and moving stops are psychology problems, not strategy problems. Your backtest assumes perfect execution.

The impact of slippage and commissions at scale (though you can model these).

Whether an edge is due to genuine market structure or statistical noise.

How Do You Backtest a Trading Strategy Step by Step?

Step 1: Define Your Strategy With Exact Rules

Before you touch any data, write down your strategy in precise, repeatable rules. No ambiguity. Someone else should be able to read your rules and take the exact same trades you would.

What to define:

Entry criteria: What specific conditions must be true for you to enter? Example: "Price touches VWAP from above, RSI is below 30, volume is above the 20-period average, and the trade occurs between 9:30 and 11:00 AM EST."

Exit criteria (target): Where do you take profit? "First target at 1:1 risk-reward, second target at previous day's high."

Exit criteria (stop): Where are you wrong? "Stop loss at the low of the setup candle, or $2 below entry, whichever is tighter."

Position sizing: How much do you risk per trade? "1% of account equity."

Filters: What conditions keep you out of a trade? "No entries during the first 5 minutes of market open. No entries within 30 minutes of a major news event."

If any of these are vague ("I'll exit when it looks like the trade is failing"), your backtest is meaningless because you'll make different decisions each time.

Dollar example: On a $50,000 account risking 1% per trade ($500), your stop distance determines your position size. If the stop is $2 below entry, you buy 250 shares. If the stop is $5 below, you buy 100 shares. Use the Position Size Calculator to calculate the exact size for each backtested trade.

Step 2: Choose Your Data Source and Time Period

Quality matters more than quantity. Backtesting against noisy, incomplete data produces unreliable results. Use a data source that provides accurate OHLCV (open, high, low, close, volume) data at the timeframe you trade.

How much data: Test across a minimum of 2 years and at least 100 trade instances. If your strategy only triggers 10 times per year, you need 10+ years of data to get a meaningful sample. The more data points, the more statistically significant your results.

Include different market conditions. Your test period should cover at least one trending market, one range-bound period, and one high-volatility event. A swing trading strategy that only works in a bull market isn't robust. You need to see how it handles choppy, sideways price action and sharp selloffs.

Step 3: Run the Backtest

There are two approaches: automated and manual.

Automated backtesting uses software to apply your rules to historical data and generate results instantly. This works well for strategies with purely objective, rule-based criteria. The software scans every bar of data, identifies qualifying setups, simulates entries and exits, and calculates performance metrics.

TradeZella offers automated no-code backtesting, so you can define your rules in plain English, run them against historical data, and see full performance metrics without leaving the platform.

Manual backtesting (also called "chart replay" or "walk-forward review") involves scrolling through historical charts bar by bar and marking each trade as you see the setup develop. This is slower but captures the nuance of discretionary strategies where context matters.

Most traders benefit from a combination: automated testing for initial strategy validation, followed by manual review of a subset of trades to verify that the setups actually look right on the chart. In TradeZella, the replay feature lets you walk through historical charts at your own pace, marking entries and exits as the chart unfolds bar by bar.

Step 4: Record and Analyze Results

Every backtested trade should be logged with the same detail as a live trade: entry, exit, P&L, setup conditions, and any notes about the trade quality.

Metric

What It Measures

Good Range

Warning Sign

Dollar Example ($50K Account)

Win Rate

% of profitable trades

40-65% (varies by style)

Meaningless without R-ratio

52% win rate = 104 winners out of 200 trades

Profit Factor

Gross profit / gross loss

Above 1.5 (solid), above 2.0 (excellent)

Below 1.0 = losing money

$38,000 gross profit / $22,000 gross loss = 1.73

Average R-Multiple

Avg return per unit of risk

+0.3R to +0.8R average

Negative = strategy loses per trade

+0.5R avg x $500 risk = $250 expected per trade

Max Drawdown

Worst peak-to-trough decline

Under 15% (manageable)

Above 25% = difficult to recover

12% max DD = $6,000 worst decline on $50K

Expectancy

Avg $ expected per trade

Positive (any amount)

Negative = no edge

$117.50/trade x 200 trades = $23,500 expected

Sample Size

Total trades in backtest

200+ trades (high confidence)

Under 100 = statistically unreliable

200 trades over 2 years = ~2 trades/day avg

Ranges are general benchmarks. Actual targets depend on strategy type (trend-following vs mean reversion) and trading timeframe. Live results typically degrade 10-20% from backtest.

Key metrics to calculate:

Win rate:What percentage of trades were profitable? For trend-following strategies, 35 to 45% is normal. For mean reversion, 55 to 65% is typical. The win rate alone means nothing without the reward-to-risk ratio.

Average R-multiple: How many R (units of risk) did each trade return on average? If your average winner is 2R and your average loser is 1R, your system is mechanically sound even at a 40% win rate.

Profit factor: Gross profit divided by gross loss. Above 1.5 is good. Above 2.0 is excellent. Below 1.0 means the strategy loses money.

Maximum drawdown: The deepest equity decline from peak to trough. This tells you how much pain you'd need to endure to trade this strategy. If the max drawdown is 15% ($7,500 on a $50,000 account), can you psychologically handle watching $7,500 disappear before the strategy recovers?

Expectancy:(Win rate x average win) minus (loss rate x average loss). This is the average expected profit per trade. Positive means the system makes money over time. Example: 45% win rate, average winner $750, average loser $400. Expectancy = (0.45 x $750) - (0.55 x $400) = $337.50 - $220 = $117.50 per trade. Over 200 trades, that's $23,500 in expected profit.

Step 5: Validate With Out-of-Sample Testing

This is where most traders skip a step and pay for it later. Out-of-sample testing means reserving a portion of your data that you didn't use during development.

How to do it: Split your data into two periods. Use the first 70% to develop and refine your strategy. Then test the final 30% without making any changes. If the strategy performs similarly on the out-of-sample data, the edge is more likely real. If it falls apart, you may have overfitted to the training data.

Walk-forward analysis is the gold standard: develop on period 1, test on period 2, then develop on periods 1+2, test on period 3, and so on. This simulates how the strategy would have performed if you'd been developing it in real time.

Monte Carlo validation: After your backtest, run a Monte Carlo simulation on the results. This randomizes the order of your trades to see how sensitive the equity curve is to trade sequence. If your strategy is profitable regardless of the trade order (across 1,000 simulations), the edge is robust. If a few unlucky sequences produce devastating drawdowns, your risk management needs adjustment.

Overfitting (curve-fitting). You tweak your strategy parameters until the backtest looks perfect on historical data. The problem: you've optimized for the past, not the future. A strategy with 15 specific conditions that produced a 90% win rate on historical data will probably fail live because it was tailored to noise, not signal. Keep your rules simple. Fewer parameters means less overfitting.

Survivorship bias. If you're backtesting stocks, make sure your data includes companies that were delisted or went bankrupt during the test period. Testing only on stocks that survived to today inflates your results because it excludes the losers.

Look-ahead bias. Using information that wasn't available at the time of the trade. Example: "I enter when the daily candle closes below the 200 MA." But in a real-time backtest, you wouldn't know the daily close until the end of the day. Make sure every decision in your backtest uses only information available at that moment.

Ignoring transaction costs. Commissions, slippage, and spread add up. A scalping strategy that returns 0.5R per trade before costs might be breakeven or negative after costs. If you're paying $5 round-trip per trade and your average win is $150, costs eat 3.3% of your gross. On 200 trades per month, that's $1,000 in friction.

Too small a sample size. 20 trades is not a backtest. It's noise. You need at least 100 trade instances for basic statistical significance, and 200+ for high confidence. If your strategy doesn't trigger often enough, test across more instruments or longer time periods.

Changing rules mid-backtest. If you see a losing streak and modify the rules to avoid those losses, you've contaminated the test. Finish the backtest with original rules, analyze the results, then make changes and run a new test from scratch.

How Do You Go From Backtest to Live Trading?

A positive backtest doesn't mean you go live at full size. The transition should be gradual:

Paper trade first. Run the strategy on live market data in a simulator for 2 to 4 weeks. This tests whether you can actually execute the rules in real time, with real market noise and real emotional pressure.

Then trade small. Start at 25 to 50% of your intended position size. Execute the strategy live for 30 to 50 trades while logging everything in your journal. Compare your live metrics to your backtest metrics.

Scale up if the data matches. If your live win rate, R-multiple, and profit factor are within a reasonable range of your backtest results (within 10 to 15%), you can increase to full size. If there's a significant gap, investigate why before scaling.

For prop firm traders: Backtest your strategy against the specific prop firm rules you'll be trading under. If your backtest shows a 12% maximum drawdown but the firm allows only 10%, your strategy needs adjustment before you pay for an evaluation. The backtest should account for the firm's daily loss limit and trailing drawdown type.

How Do You Track Backtested Strategies in Your Journal?

The backtest gives you your expected metrics. Your trading journal gives you your actual metrics. Comparing the two is how you know whether the strategy is working live or degrading.

Create a Strategy in TradeZella for each backtested setup. Tag every live trade with its Strategy name. After 30 live trades, pull up the per-setup analytics and compare:

Backtest win rate vs live win rate. If your backtest showed 52% and you're running at 43% live, something is different. Either market conditions changed, or you're not executing the rules exactly.

Backtest R-multiple vs live R-multiple. If your backtest average was +1.4R and your live average is +0.8R, you might be cutting winners short or letting losers run past your stop.

Backtest profit factor vs live profit factor. This is the single best comparison metric. A backtest profit factor of 1.8 that degrades to 1.3 live is normal (10 to 20% degradation). A backtest of 1.8 that degrades to 0.9 live means something is fundamentally broken.

Use habit tags to mark trades where you deviated from the backtested rules. After 50 trades, compare P&L on "followed rules" trades vs "deviated" trades. This tells you whether the degradation is the strategy's fault or yours.

Your weekly trade review should include a backtest comparison check: are your live metrics tracking your backtested expectations? If yes, keep executing. If no, diagnose whether it's market conditions, execution, or rule drift.

Key Takeaways

Backtesting validates whether a strategy has a historical edge before you risk real capital. It doesn't guarantee future results, but it eliminates strategies with no basis.

Define your strategy with exact, unambiguous rules before testing. Vague criteria produce unreliable results.

Test across at least 2 years and 100+ trade instances covering different market conditions (trending, range-bound, high-volatility).

Calculate win rate, profit factor, average R-multiple, max drawdown, and expectancy to evaluate your results.

Use out-of-sample testing and Monte Carlo simulation to verify your results aren't overfitted to historical data.

Transition from backtest to live trading gradually: paper trade, then trade small (25 to 50% size), then scale up based on data.

Track backtested strategies in your journal with setup tags. Compare live metrics to backtest metrics after 30+ trades to verify the edge is real.

Expect 10 to 20% degradation from backtest to live trading. Anything worse than that needs investigation.

Frequently Asked Questions

What is backtesting in trading?

Backtesting is the process of applying a trading strategy to historical market data to measure how it would have performed. You define exact entry and exit rules, run those rules against past price data across hundreds of trades, and calculate key metrics like win rate, profit factor, expectancy, and maximum drawdown. A positive backtest gives you statistical evidence of an edge before risking real capital.

How many trades do I need in a backtest for reliable results?

A minimum of 100 trades provides basic statistical significance. For higher confidence, aim for 200 to 500 trades. If your strategy triggers rarely, extend the testing period or test across additional instruments to build a larger sample. Twenty trades is not a backtest. It's noise. You need enough data points to distinguish between genuine edge and random luck.

Can I backtest discretionary strategies?

Yes, using manual chart replay. Scroll through historical data bar by bar and mark entries and exits as you identify setups. This is slower than automated backtesting but captures the subjective elements of discretionary trading. Log every trade with the same detail you'd use for a live trade: entry, exit, P&L, R-multiple, setup conditions, and notes about trade quality.

How do I know if my backtest results are overfitted?

Run out-of-sample testing: reserve 30 percent of your data and test the strategy without modifications. If results degrade significantly compared to your development period, you likely overfitted. Also, be skeptical of strategies with many specific parameters. More than 3 to 5 conditions increase overfitting risk. If your strategy needs 12 conditions to be profitable, it's almost certainly curve-fit to historical noise.

What is a good profit factor for a backtested strategy?

A profit factor above 1.5 is solid. Above 2.0 is excellent. Below 1.0 means the strategy loses money. Keep in mind that live trading typically degrades backtest metrics by 10 to 20 percent due to slippage, emotional decisions, and execution differences. A backtest profit factor of 1.8 might run at 1.4 to 1.6 in live trading, which is still profitable.

What is the difference between in-sample and out-of-sample testing?

In-sample data is the historical period you use to develop and refine your strategy. Out-of-sample data is a separate period you reserved and did not look at during development. Testing your strategy on out-of-sample data without making changes shows whether the edge generalizes beyond the data you trained on. If the strategy works on both datasets, the edge is more likely real. If it only works on the in-sample data, you probably overfitted.

How long should I paper trade before going live?

Paper trade your backtested strategy for 2 to 4 weeks or 30 to 50 trades, whichever comes first. The purpose is to verify that you can execute the rules in real time with live market data. Compare your paper trading metrics to your backtest metrics. If they're within 10 to 15 percent, move to live trading at 25 to 50 percent of your intended position size. If there's a bigger gap, continue paper trading until you identify why.