Last Updated: July 06, 2026

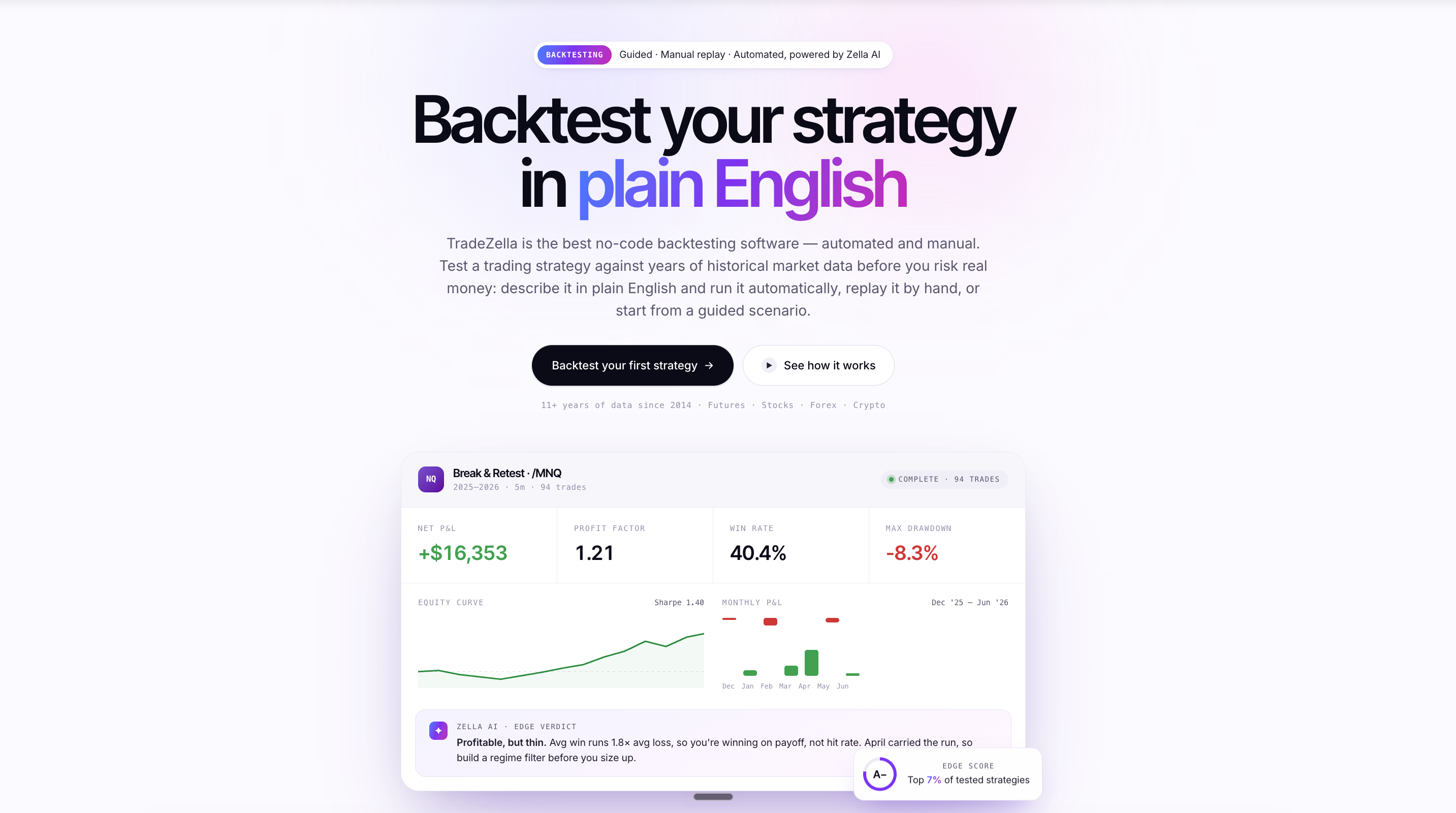

Automated backtesting is the process of testing a trading strategy against historical market data using software that executes the rules automatically, without the trader manually stepping through each bar. Instead of replaying charts one candle at a time and deciding whether to enter or exit, traders write their entry and exit conditions in plain English or code, and the backtesting engine applies those rules across months or years of data in seconds. Every trade is logged, every result is recorded, and the final output is a complete performance report with metrics like win rate, profit factor, and maximum drawdown.

Until recently, automated backtesting required coding in Python, Pine Script, or MQL5. Most retail traders either paid someone to build their tests or gave up entirely and stuck with manual chart replay. That barrier is disappearing. Platforms like TradeZella now let you write rules in plain English and get results in minutes, making automated backtesting accessible to traders who have never written a line of code.

This guide covers how automated backtesting works, what you can test, how to read results, how to avoid the biggest dangers like overfitting, and why most traders are making the switch from manual chart replay.

TL;DR

Automated backtesting writes your trading rules into software that tests them across years of data in minutes. It eliminates forward bias, generates large sample sizes, and tells you whether a strategy has a real edge before you risk money. TradeZella has automated backtesting with plain English rules, no coding required.

How Does Automated Backtesting Work?

The concept behind automated backtesting is straightforward. You define the rules. The software does the work. Here is how it breaks down step by step.

Step 1: Define your rules. You write the exact conditions for entering a trade, exiting a trade, placing a stop loss, and sizing your position. Depending on the platform, this happens in code (Pine Script, Python, MQL5) or in plain English. For example: "Buy when the 9 EMA crosses above the 21 EMA and RSI is below 30 on the 5-minute chart. Set a stop loss at 1.5 ATR below entry. Take profit at 2R."

Step 2: The software scans historical data. The backtesting engine moves through historical price data bar by bar, checking every candle against your rules. When the conditions are met, it "takes" the trade, recording the entry price, time, and all relevant parameters.

Step 3: Every trade is tracked. Each simulated trade is logged with entry price, exit price, stop loss, profit or loss in both dollars and R-multiples, hold time, and the exact conditions that triggered entry and exit. On a $50,000 account risking $500 per trade, a 2R winner shows as +$1,000 and a 1R loser shows as -$500.

Step 4: The software generates results. After scanning the full dataset, the engine produces a complete performance report. You see total trades, win rate, profit factor, expectancy, maximum drawdown, consecutive losses, and the full trade log. Every individual trade is visible, not just summary statistics.

Step 5: You analyze and decide. With the results in front of you, you determine whether the strategy has a genuine edge or is producing random noise. If profit factor is above 1.3 and expectancy is positive across 200+ trades, you have statistical evidence that the strategy works. If the numbers are marginal, you refine the rules and test again.

The critical difference from manual testing: no human judgment is involved during execution. The software applies your rules with perfect consistency, eliminating the forward bias that plagues manual replay. It does not "know" what happens next. It does not skip boring setups. It does not unconsciously avoid losses.

To put the speed advantage in perspective, results appear in minutes with automated backtesting. The same test done manually, replaying each bar and making each entry and exit decision, takes 40 to 80 hours spread across two months. That is the difference between validating an idea before the market opens tomorrow and spending an entire quarter on one test.

Why Is Manual Backtesting Dying?

Manual backtesting served traders well for decades. You load a chart, hide future bars, step through candle by candle, and record each trade on a spreadsheet. It taught discipline, built pattern recognition, and forced traders to engage with price action. But it has fundamental problems that automated testing solves, and those problems are driving the shift.

Forward bias destroys accuracy. This is the single biggest issue with manual backtesting. When you replay a chart, your eyes naturally drift to the right side of the screen. You catch a glimpse of the next few bars. You subconsciously avoid trades that you know will lose. Studies and trader reports consistently show that forward bias inflates manual backtest win rates by five to fifteen percent. A strategy that looks like a 55 percent winner in manual testing might actually run at 42 percent live. On a $50,000 account risking $500 per trade, that gap turns a profitable system into a losing one. Your how to backtest a trading strategy guide covers bar replay techniques that reduce this bias, but automated testing eliminates it entirely.

Time cost kills sample size. A thorough manual backtest of 100 trades takes 40 to 80 hours depending on strategy complexity and timeframe. Most traders quit at 30 to 50 trades because the process is tedious. That sample size is statistically insufficient for confident conclusions. You need at least 50 trades for basic viability, 100 for solid confidence, and 200 or more for robust validation. Automated backtesting generates hundreds of trades in minutes, making large sample sizes practical instead of theoretical.

Human inconsistency creeps in. On trade number 5, you apply your rules precisely. On trade number 80, you are tired and start cutting corners. By trade number 120, your interpretation of "a clean pullback to the moving average" has shifted without you noticing. The rules you applied at the end of the test are not the same rules you applied at the beginning. Automated testing applies your rules with perfect consistency from trade 1 through trade 1,000.

Optimization is impractical. What if you want to test your strategy with a 1.5 ATR stop instead of a 2 ATR stop? Or test it during the first hour of the session versus the full day? Each variation means repeating the entire manual process. Five variations means five times the work. Automated backtesting runs all five in minutes, letting you compare results side by side and find the conditions where your strategy performs best.

Multi-instrument testing is nearly impossible. Testing one strategy across ES, NQ, CL, and GC manually takes four separate multi-week sessions. With automated testing, you run each instrument as a separate test and get results in minutes rather than months.

That said, manual testing is not completely dead. It still serves specific purposes. Manual bar replay is valuable for execution practice, especially for discretionary traders who need to develop their screen-reading skills. It builds price action intuition that no automated test can replicate. And for strategies with strong discretionary components ("the pullback looks clean" or "volume confirms the breakout"), manual testing captures nuance that rule-based automation cannot. The best approach is often both: automated testing for statistical validation, then manual replay for execution refinement. For a deeper side-by-side analysis, see our manual vs automated backtesting comparison.

What Can You Test With Automated Backtesting?

TradeZella has automated backtesting that lets you write rules in plain English, run them across years of historical data, and see every individual trade with full analytics. No coding required. Here is what you can test with it.

Entry conditions. Indicator crossovers (9 EMA above 21 EMA), price levels (break above yesterday's high), pattern triggers (inside bar breakout), candlestick formations (engulfing bar at a key level), and multi-condition setups (RSI below 30 AND price above VWAP AND within the first 30 minutes of the session). If you can write it as a condition, you can test it. For specific patterns you might test, see our guide on trading patterns.

Exit conditions. Fixed profit targets (2R, 3R), trailing stops (move stop to breakeven after 1R, trail at 1 ATR), time-based exits (close at 3:30 PM regardless of P&L), indicator reversals (exit when RSI crosses above 70), and partial exits (sell half at 1R, let the rest run to 3R). Each of these is testable, and the results show you which exit method maximizes your expectancy on a $50,000 account.

Stop loss methods. Fixed percentage stops, ATR-based stops (1.5 ATR below entry), structure-based stops (below the prior swing low), and time-based stops (exit if the trade has not hit 1R within 45 minutes). You can test each method against the same entry conditions and see which produces the highest profit factor. Our stop loss strategies guide covers five methods in depth.

Position sizing rules. TradeZella offers three position sizing options: fixed contracts, risk percentage of running balance (which compounds as the account grows), and fixed dollar risk per trade. On a $50,000 account, you might set risk at one percent ($500 per trade) using the risk percentage method, or set a flat $500 using fixed dollar risk. The impact on terminal account value is often dramatic. One percent fixed risk on a $50,000 account with a 0.25R expectancy produces very different results than two percent risk on the same strategy. See our risk per trade guide for the math.

Trading days and trading sessions. The automated backtesting setup lets you select which trading days to include and which trading sessions to test (regular trading hours, pre-market, after-hours, or specific session windows). These filters frequently reveal that a mediocre full-session strategy becomes excellent when restricted to its best hours. On a $50,000 account, filtering a strategy to its strongest session window might improve profit factor from 1.1 to 1.8 while cutting trade count in half.

Instrument-specific testing. Run the same strategy on different stocks, forex pairs, or futures contracts by running a separate backtest for each instrument. Test your breakout strategy on ES, then on NQ, then on CL to see which instruments it performs best on. Each test runs in minutes, so comparing across instruments is fast even though you test one symbol at a time. For forex-specific testing considerations like session behavior and spread impact, see our forex backtesting guide.

Market condition awareness. By running the same strategy across different date ranges covering trending, ranging, and volatile markets, you can see how conditions affect performance. Testing the same strategy across different market environments shows you when to deploy it and when to sit on the sidelines.

What you cannot test. Purely discretionary judgment. If your edge is "the chart looks bullish" or "I can feel that this level will hold," there is no way to code that into a rule. Tape reading, screen watching, and gut-feel entries require manual testing or live validation. For strategies with heavy discretionary components, our backtest without code guide shows how to use journal-based validation instead.

What Is the Difference Between Automated Backtesting and Algorithmic Trading?

This is one of the most misunderstood distinctions in trading. Many traders hear "automated" and assume it means a bot is placing trades for them. That is not what automated backtesting is.

Automated backtesting is testing a strategy on historical data. No real money is at risk. No trades are placed in the market. The software simulates what would have happened if you had traded those rules over a specific period. The output is a performance report that tells you whether the strategy has a statistical edge. It is a research tool.

Algorithmic trading is executing trades automatically in live markets with real money. An algorithm monitors real-time data, identifies setups that match its rules, and places orders without human intervention. The output is actual positions in your brokerage account. It is an execution tool.

TradeZella does automated backtesting, not algorithmic trading. It tests your ideas so you can trade them manually with confidence. For most retail traders, this is actually the better approach. You keep full control over execution. You can apply discretionary judgment on top of your validated rules. You do not need to worry about API connections to your broker, latency issues, or an algorithm making decisions while you sleep.

The workflow looks like this: automated backtesting validates the edge (does this strategy produce a positive expectancy across 200 trades?), then you trade it manually with the confidence that the numbers support your approach, then your trading journal tracks live results. Over time, you can review your journal metrics alongside the backtest metrics to see whether performance is holding. If live results are in the same range as the backtest, the edge is confirmed. If they diverge significantly, something has changed and you investigate.

Think of automated backtesting as the R&D department. Algorithmic trading is the factory floor. Most traders need R&D. They need to know whether their strategy actually works before risking real money on it. TradeZella gives you that answer in minutes instead of months.

How Do You Write Rules for Automated Backtesting?

The quality of your automated backtest depends entirely on the quality of your rules. Vague rules produce unreliable results. Precise rules produce actionable data. Here is how to write rules that generate meaningful backtests.

The traditional approach: code. For years, automated backtesting required programming. Pine Script for TradingView, Python with libraries like backtrader or zipline, NinjaScript for NinjaTrader, MQL5 for MetaTrader. Each language has a learning curve. Most retail traders spend weeks learning to code before running their first backtest, and many give up before finishing. The code approach is powerful but creates a barrier that keeps most traders stuck with manual testing.

The plain English approach. TradeZella's automated backtesting removes the coding barrier entirely. You write your rules in plain English. Instead of writing 40 lines of Pine Script, you write: "Buy when the 9 EMA crosses above the 21 EMA on the 5-minute chart. RSI must be below 30. Only trade during RTH. Stop loss at 1.5 ATR below entry. Target 2R." The backtesting engine interprets your rules and applies them to historical data. No syntax errors. No debugging. No Stack Overflow searches at midnight.

Pre-built templates. For traders who want to test proven concepts before building their own rules, TradeZella offers pre-built templates covering popular strategies including ICT concepts, Opening Range Breakout, trend following, and mean reversion. Each template is editable, so you can modify conditions to match your specific approach.

The 6-step rule construction framework. Regardless of whether you use plain English or code, every automated backtest rule set follows the same structure:

- Choose your instrument. ES futures, NQ, a specific stock, a forex pair. Be specific.

- Set your timeframe. 1-minute, 5-minute, 15-minute, daily. Match the timeframe to your trading style.

- Define entry conditions. What has to happen for you to buy or sell? Use specific indicators and levels.

- Define exit conditions. Profit target (in R-multiples or fixed points), stop loss placement, and any time-based exits.

- Set risk parameters. Choose your position sizing method: fixed contracts, risk percentage of running balance, or fixed dollar risk per trade ($500 on a $50,000 account).

- Add filters. Select which trading days to include and which trading sessions to test (RTH only, specific session windows, or the full day).

Common rule-writing mistakes. Too many conditions leads to curve fitting. If your entry requires 8 indicators to align, you have probably matched historical noise rather than a genuine pattern. Too few conditions produces noisy results with no real edge. Contradictory filters (like requiring RSI below 30 AND above 70) produce zero trades. The sweet spot is typically 3 to 5 conditions that define a clear, repeatable setup.

Dollar example: simple vs complex. A simple rule set on a $50,000 account (EMA crossover + RSI filter + 2R target) might produce 180 trades over one year with a 1.4 profit factor and +0.22R expectancy. That translates to roughly $19,800 in expected profit. A complex 8-condition version of the same strategy might produce 35 trades with a 2.1 profit factor, but the sample size is too small and the rules are almost certainly overfit. Simplicity wins. For the full guide to building and running your first backtest with TradeZella, see backtest without code.

What Metrics Should You Look For in Automated Backtest Results?

Running an automated backtest is the easy part. Reading the results correctly is what separates traders who build lasting edges from traders who blow up chasing illusions. Here are the metrics that matter and what the numbers should look like.

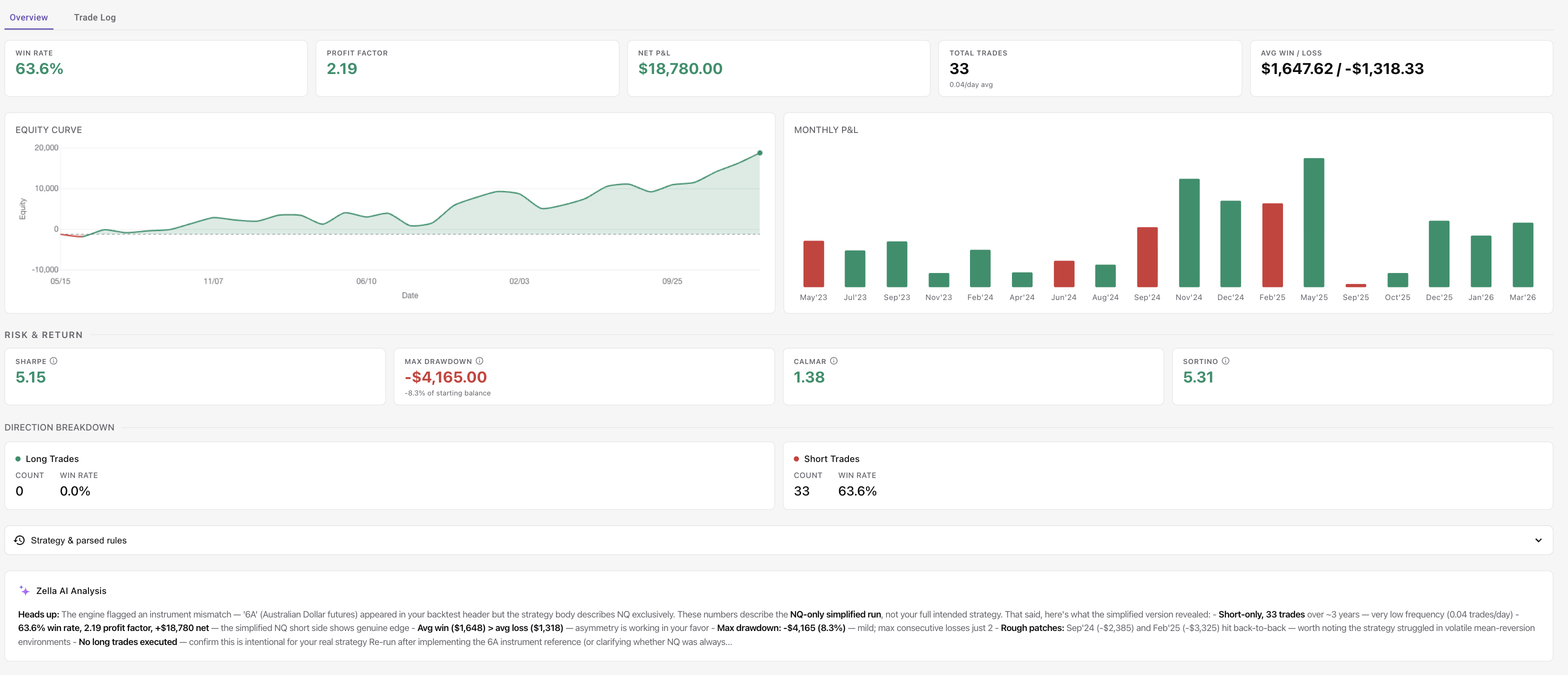

Win rate. The percentage of trades that were profitable. A common misconception is that you need a high win rate to be profitable. You do not. A strategy with a 40 percent win rate and a 3:1 average winner to average loser ratio is highly profitable. On a $50,000 account risking $500 per trade across 200 trades, a 40 percent win rate with a 3:1 ratio produces 80 winners at $1,500 each ($120,000) and 120 losers at $500 each ($60,000), for a net profit of $60,000. Context matters more than the number itself.

Profit factor. Gross profit divided by gross loss. A profit factor of 1.0 means breakeven. Below 1.0 means losing money. Above 1.0 means profitable. The benchmark for a viable strategy is 1.3 or higher. Anything above 2.0 on a sample of 200+ trades is excellent. If your backtest shows a profit factor of 4.0 or above, be suspicious. That usually signals overfitting rather than a genuine edge.

Expectancy. The average R-multiple per trade. This is the single most important number in your backtest. Positive expectancy means the strategy produces money over time. On a $50,000 account with $500 risk per trade, an expectancy of +0.25R means you expect to earn $125 per trade on average. Across 200 trades, that is $25,000. Even small positive expectancy compounds meaningfully over hundreds of trades.

Maximum drawdown. The worst peak-to-trough decline during the test period. This tells you the psychological and financial pain you need to survive while trading the strategy live. If the backtest shows a 15 percent maximum drawdown on a $50,000 account ($7,500), you should expect similar or worse drawdowns in live trading. If you cannot tolerate that drawdown emotionally or financially, the strategy is not right for you, regardless of its expectancy.

Sample size. The number of trades in the backtest. This determines how much confidence you can place in the other metrics. Below 30 trades, the results are essentially random. At 50 trades, you have basic viability. At 100 trades, you have solid confidence. At 200 or more, you have robust statistical validation. Automated backtesting makes large sample sizes practical because generating 200 trades takes minutes instead of months.

Consecutive losses. The maximum number of losing trades in a row. This prepares you psychologically for live trading. If the backtest shows a maximum losing streak of 8, you will experience something similar (or worse) live. On a $50,000 account risking $500 per trade, 8 consecutive losses means a $4,000 drawdown (8 percent) from that streak alone. Know this number before you trade live.

Risk-reward ratio. The average winning trade divided by the average losing trade, expressed in R-multiples. A ratio of 2:1 means your average winner is twice your average loser. This ratio interacts directly with win rate: a 2:1 ratio needs only a 33.3 percent win rate to break even. Check whether your backtest's actual ratio matches your planned ratio. If you designed the strategy for 2:1 but the backtest shows 1.3:1, something is wrong with your exit rules.

What Is the Best Automated Backtesting Software?

Choosing the right platform depends on your technical ability, the markets you trade, and how you plan to use the results. Here is a brief overview of the major options. For a detailed head-to-head breakdown, see our full best backtesting software comparison.

TradeZella. Plain English rules, no coding required. Every individual trade visible in the results. Pre-built templates for ICT, Opening Range Breakout, trend following, and mean reversion strategies. Zella AI analyzes the results and identifies patterns you might miss. Full journal integration means your backtesting, live trade logging, and analytics all live in the same platform. Supports ES, NQ, CL, GC, MES, MNQ, forex pairs, stocks, and more. For the full product walkthrough, see backtest with TradeZella.

TradingView (Pine Script). Free to start, massive community with thousands of shared scripts, and a powerful charting platform. But automated backtesting requires learning Pine Script, a proprietary programming language. No journal integration. No AI analysis. No connection to your live trading data. Good for coders. Poor for traders who want to test and trade, not test and code.

Python (backtrader, zipline, Lean). Maximum flexibility. You can test literally anything with enough code. But the learning curve is steep. Setting up a Python backtesting environment from scratch takes days. Debugging logic errors takes longer. No journal integration. Best for quantitative traders with programming backgrounds.

NinjaTrader (NinjaScript). Strong for futures traders. Requires C# coding. Powerful execution and data capabilities. But building a custom strategy in NinjaScript takes significant development time, and there is no built-in journal or AI analysis.

MetaTrader 5 (MQL5). The standard for forex backtesting. Requires MQL5 coding. Large marketplace of pre-built expert advisors. Built-in strategy tester with optimization capabilities. But limited to forex and CFDs, no journal integration, and the coding barrier remains.

QuantConnect (Lean). Institutional-grade, cloud-based, supports Python and C#. Research-notebook environment for iterative testing. But the learning curve is significant, the interface is designed for quants, and retail traders often find it overwhelming.

Why TradeZella is different. Most platforms require you to be either a coder or a manual tester. TradeZella lets you be a trader. Write rules in plain English, run them in minutes, see every individual trade with full details, and get AI-powered analysis of your results. The same platform also handles your live journal, analytics, and replay, so your entire workflow lives in one place. For a head-to-head comparison with another popular replay-based platform, see our FX Replay vs TradeZella breakdown.

Automated Backtesting for Prop Firm Traders

Automated backtesting is especially valuable if you trade prop firm trading evaluations. Instead of paying a $300 to $600 evaluation fee and discovering your strategy cannot meet the firm's rules, you can test beforehand. Set the daily loss limit to match the firm (typically 3 to 5 percent), set maximum drawdown to match (5 to 10 percent), and add consistency targets if the firm requires them (Topstep's best-day cap, for example). If the automated backtest shows your strategy violating the firm's daily loss limit on 12 out of 200 trading days, you know to adjust before spending money on the evaluation.

On a $100,000 funded account with a $5,000 daily loss limit, a strategy that occasionally produces $6,000 losing days needs modification. Automated backtesting shows you exactly how often those violations occur and what changes (smaller position size, tighter stops, fewer trades per day) bring the risk within limits. For a step-by-step guide to evaluations, see how to pass your prop firm challenge.

How Zella AI Analyzes Your Automated Backtest Results

Running the backtest gives you data. Zella AI, TradeZella's built-in AI trading partner, turns that data into insights you would not find on your own.

Zella AI breaks your backtest results by hour and session, showing you that your EMA crossover strategy produces a 1.8 profit factor between 9:30 AM and 11:00 AM but drops to 0.7 after lunch. Without this analysis, you would trade the strategy all day and dilute your edge with afternoon noise. On a $50,000 account, restricting to your best hours might cut your trade count from 200 to 90 while improving net profit by 40 percent.

Every individual trade is visible. Unlike platforms that only show summary statistics, TradeZella displays every single trade the backtest generated. You can see the exact entry price, exit price, hold time, R-multiple result, and the conditions that triggered each trade. This transparency lets you review specific trades that concern you, spot patterns in losses, and verify that the engine is applying your rules correctly. On a $50,000 account, scrolling through 200 trades and seeing the actual price action behind each one builds confidence that the results are real, not just numbers on a screen.

Zella AI's AI trading agents also enhance the broader testing workflow. The Auto-Tagger applies your tagging criteria to every trade automatically, keeping your data clean and consistent. The Session Review agent compares your daily plan against actual results, catching drift between what you tested and how you are actually trading. The Market Sentiment Briefing generates a pre-market plan based on your configured strategy and instruments, connecting your backtested edge to each day's preparation.

Key Takeaways

- Automated backtesting tests your strategy against years of data in seconds. You define rules, the software applies them with perfect consistency, and you get a complete performance report without manually replaying a single chart.

- It eliminates forward bias. The number one problem with manual backtesting, accidentally seeing future price data, does not exist when software applies rules bar by bar without human involvement.

- Sample size goes from impractical to easy. Manual testing caps most traders at 30 to 50 trades. Automated testing generates 200+ trades in minutes, giving you statistical confidence in your results.

- It is not algorithmic trading. Automated backtesting tests your ideas. You still trade manually. TradeZella validates the edge so you can execute with confidence.

- Plain English rules remove the coding barrier. TradeZella lets you write rules in plain English instead of Pine Script, Python, or MQL5. Pre-built templates for ICT, ORB, trend following, and mean reversion give you starting points.

- The metrics that matter are profit factor, expectancy, maximum drawdown, and sample size. Profit factor above 1.3, positive expectancy, survivable drawdown, and 200+ trades is the benchmark.

- Zella AI adds depth to your results. AI-powered analysis identifies time-of-day patterns and surfaces insights from your backtest data that you might miss reviewing the numbers alone.

- Automated backtesting is the starting point for finding your trading edge. Test the idea, validate the numbers, trade it live, and track the results.

Frequently Asked Questions

What is automated backtesting in simple terms?

Automated backtesting is a way to test whether a trading strategy would have made money in the past. You write your trading rules, and software applies them to historical market data automatically. Instead of manually replaying charts bar by bar, the software scans months or years of price data in seconds and generates a complete report showing every trade the strategy would have taken, including win rate, profit factor, and maximum drawdown. It is a research tool that validates your trading ideas before you risk real money.

Do I need to know how to code?

Not with TradeZella. Traditional automated backtesting platforms like TradingView, NinjaTrader, and MetaTrader require you to write code in languages like Pine Script, C#, or MQL5. TradeZella lets you write your rules in plain English instead. You describe your entry conditions, exit conditions, stop loss placement, and position sizing in natural language, and the backtesting engine interprets and applies them. Pre-built templates for popular strategies like ICT setups, Opening Range Breakouts, and trend following are also available as starting points.

Can I use automated backtesting for day trading and swing trading?

Yes. Automated backtesting works across all trading styles and timeframes. Day traders can test strategies on 1-minute, 5-minute, or 15-minute charts with session filters restricting trades to their best hours. Swing traders can test on daily or 4-hour charts with multi-day holding periods and overnight gap handling. The same strategy can be tested across different timeframes to see where it performs best. On a fifty thousand dollar account, a scalping strategies backtest might generate 500 trades over six months on a 1-minute chart, while a swing trading test on the daily chart might produce 60 trades over the same period. Both are valid if the sample size meets minimum thresholds.

What is the difference between automated backtesting and paper trading?

Automated backtesting tests a strategy on past data. Paper trading tests a strategy on current data in real time, without real money. They serve different purposes in the validation process. Backtesting answers the question "did this strategy work historically?" across hundreds or thousands of trades in minutes. Paper trading answers the question "can I execute this strategy in real time?" across twenty to thirty trades over several weeks. The recommended workflow is automated backtesting first (to validate the edge exists), then paper or reduced-size live trading (to validate your execution), then full-size live trading once both stages confirm the strategy works.

What should you look for in automated backtesting software?

The best automated backtesting software lets you test without writing code, shows every individual trade rather than just summary statistics, and gives you enough historical data to reach a meaningful sample size. Look for plain-English rule input so you do not need to learn a programming language, individual trade visibility so you can verify the results, several years of data across the markets you trade, and AI analysis that turns raw numbers into insights. Integration with a journal matters too, so your backtests and live trades sit in one place. TradeZella covers all of these: plain-English rules, every trade visible with the setup drawn on the chart, more than 11 years of data across stocks, forex, futures, and crypto, Zella AI analysis, and a built-in journal.

How does TradeZella's automated backtesting work?

TradeZella's automated backtesting lets you write trading rules in plain English and run them across years of historical market data. You select an instrument (stocks, futures, or forex), set a timeframe, write your entry and exit conditions in natural language, and the engine scans the data bar by bar. Every individual trade is visible in the results, not just summary statistics. The analytics dashboard shows win rate, profit factor, expectancy, maximum drawdown, and more. Zella AI, TradeZella's built-in AI trading partner, analyzes the results to identify time-of-day patterns and surface insights you might miss reviewing the data on your own.

What makes TradeZella's automated backtesting different from other tools?

Most automated backtesting tools make you choose between coding (TradingView's Pine Script, NinjaTrader's C#, MetaTrader's MQL5) and a menu-based condition builder. TradeZella lets you write the strategy in plain English, no code and no dropdowns, and it is the only one that connects backtesting to a full journal. Every individual trade is visible, and the AI draws the exact setup it traded on each chart, the Fair Value Gap, the liquidity sweep, or the breaker block and its retest, so you see why each trade was taken. Results feed 50+ analytics reports, and because TradeZella imports trades from 500+ brokers, you can compare your backtest against your live results in one dashboard. Built-in ICT indicators and Zella AI analysis round it out.